The Non-Financial Reporting Directive: What You Need To Know

Does your company have offices within the European Union (EU) with over 500 members of staff*? If yes, pay close attention to this blog – because it can help your business navigate a changed regulatory environment.

*Or 250 members if based in Sweden or Finland, or 10 if based in Greece.

The Regulatory Space for Non-Financial Disclosure is Blowing Up

It’s not an exaggeration to say the regulatory space is blowing up on non-financial disclosure. The NFR Directive is just one of the 4,000+ initiatives globally that require or recommend disclosure on non-financial issues – and this number is rising at a high speed.

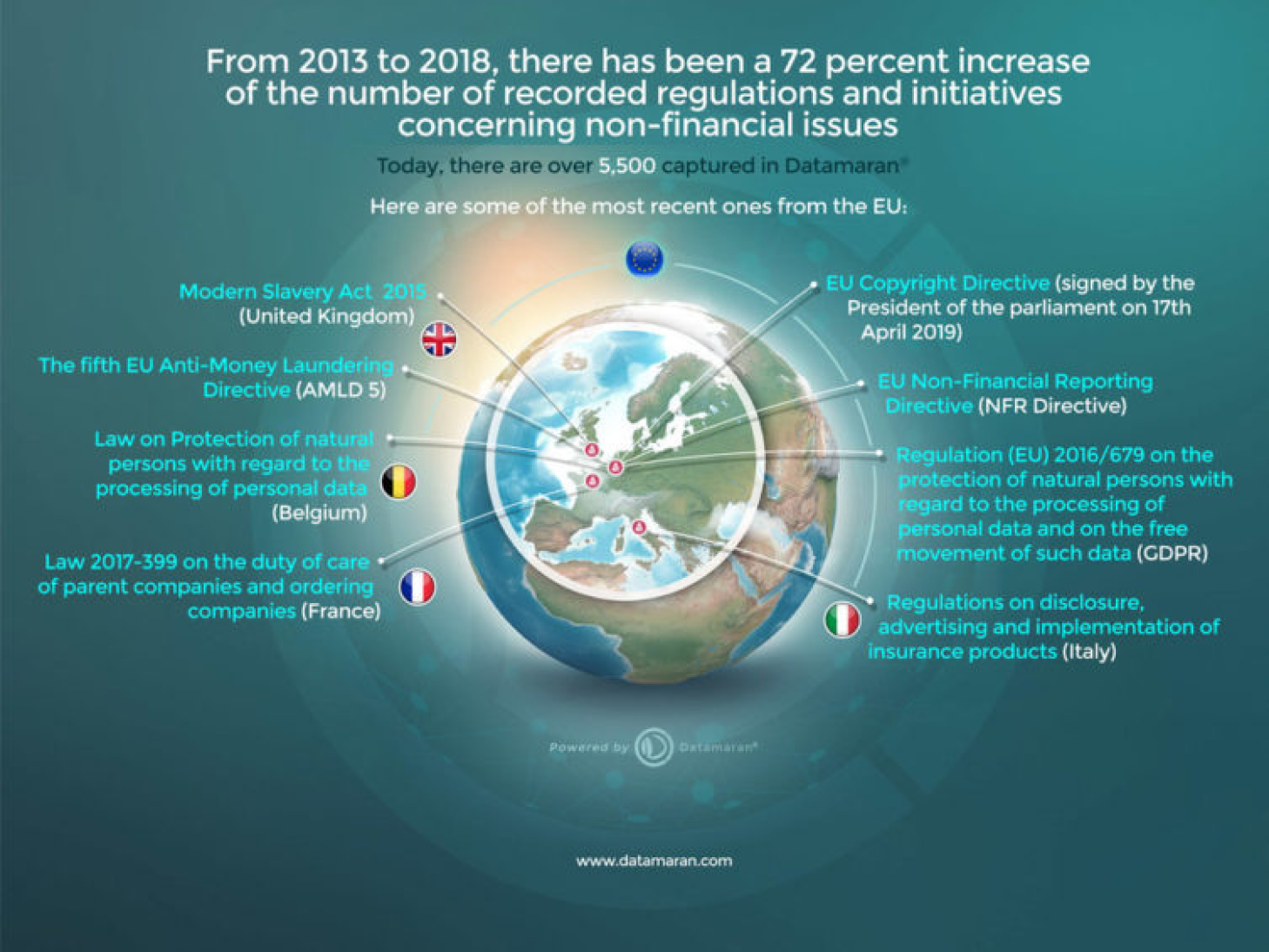

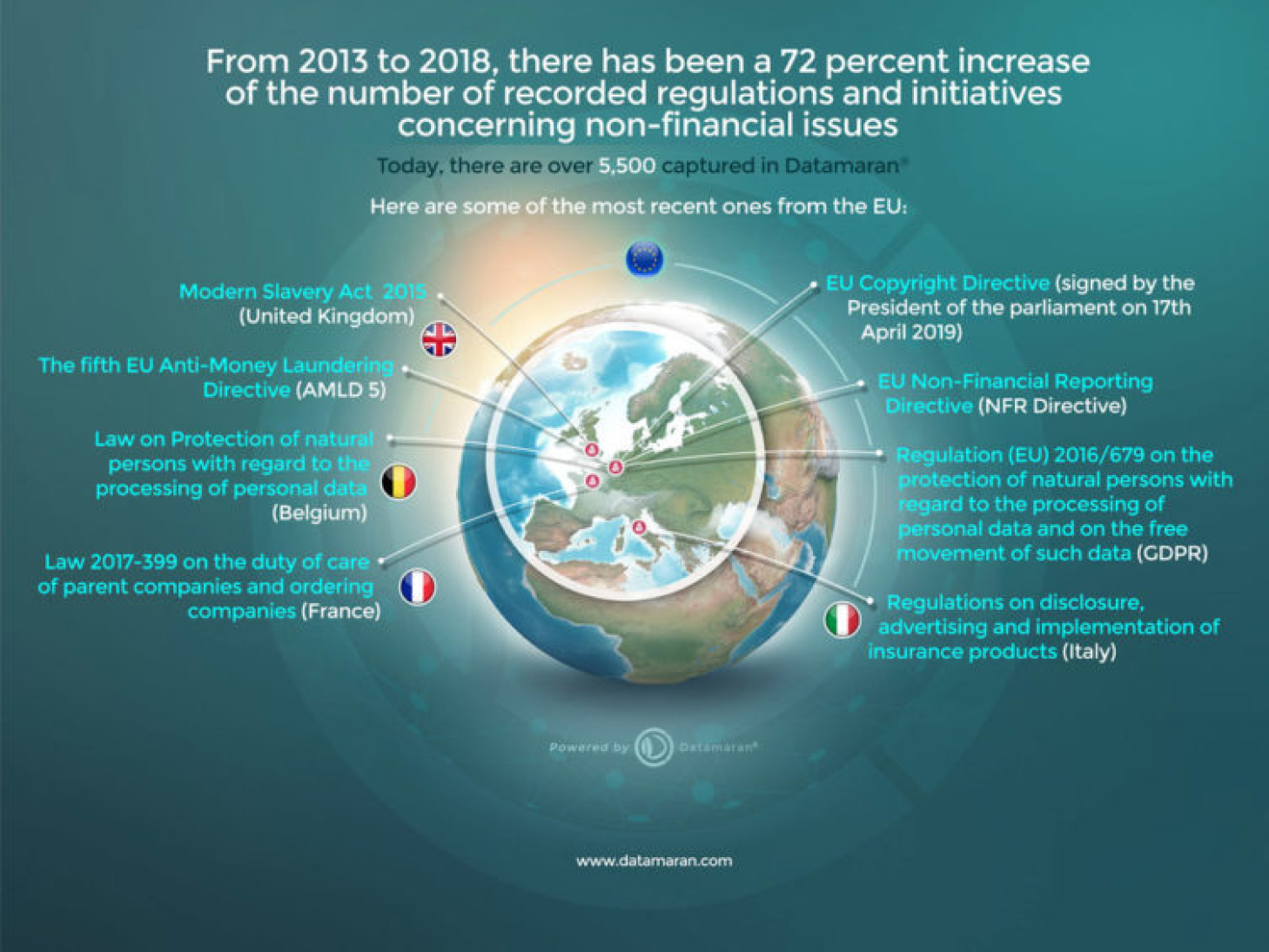

According to Datamaran's Global Insights Report, from 2013 to 2018 there has been a 72 percent increase in the number of recorded regulations concerning non-financial issues. And this trend looks set to continue.

{kind=link}

Recently, organizations such as: the TCFD, The World Economic Forum, The World Federation of Exchanges (WFE), and a joint work by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) and the World Business Council for Sustainable Development (WBCSD) – have all published their recommendations on how they expect companies to manage and disclose their non-financial risks.

The NFR Directive is a leading example of how the landscape has changed – and continues to change. The evolution of accountability shows us it is only a matter of time before prominent voluntary initiatives will become mandatory regulations, as such being ahead of the curve will help business mitigate any backlash.

Companies of much smaller size are impacted by the NFR Directive too. Business who fails to take note of the change are leaving themselves exposed.

Additionally, if part of your supply chain is based in the EU but the entities operating within do not comply with the EU Directive, this could have knock on effects for your business.

Companies must not only provide more granular information on non-financial risks and opportunities within their own operations, they must also consider these across their value chain.

A recent French law – “the duty of care of parent companies” or “devoir de vigilance des entreprises donneuses d'ordre” is a landmark example of how regulators are demanding more information from companies. For the first time, a National Government is requiring that large companies assess and address adverse impacts across their supply chain.

Coming into force in March 2018, “the duty of care of parent companies” gives us a sense of what is to follow in the next decade.

The Rising Cost of Non-Financial Risk

So, what happens if companies do not comply with these laws?

As it can be seen in the infographic below, the top 10 banks globally lost $200bn through litigation compensation claims and organizational mishaps related to non-financial issues between 2008 and 2012.

{kind=link}

The infographic above also shows that there is a disparity between the percentage of companies that believe themselves to be prepared for the EU Directive, and the percentage of investors who believe companies are prepared.

This highlights a gap between the level of detail companies provide and investor expectations.

The question is how can your company get ahead of these rising risks and opportunities?

So, What is the Non-Financial Reporting Directive?

The directive requires public disclosure documents such as annual reports, sustainability reports, and integrated reports to include the below topics. You need to ensure you are disclosing the impacts of your business activities on issues that fall into the following categories:

- Environmental matters

- Social and employee aspects

- Respect for human rights

- Anti-corruption and bribery issues

- Diversity on board of directors.

The disclosure must include a description of the company’s business model, a description of the policies adopted regarding the listed issues, the outcome of said policies, the risks related to those matters linked to the company’s operations, and non-financial key performance indicators relevant to the particular business (as referenced within the NFR Directive).

The Directive applies a “comply or explain” system, meaning if no policy is in place in one of the above matters, your company must explain the reasons behind this. The “comply or explain” principle ensures that if a company does not apply a policy regarding these issues, it will be disclosed publicly, encouraging companies to address this gap, in order to avoid negative publicity.

Update:

What is the Corporate Sustainability Reporting Directive (CSRD)?

On April 21st 2021, the European Commission launched their proposal for a Corporate Sustainability Reporting Directive (CSRD), which will amend the existing reporting requirements included in the NFRD. In particular, the new proposal:

Requires the audit of reported information (limited level of assurance);

In addition, the Corporate Sustainability Reporting Directive (CSRD) will mandate over 50,000 companies in Europe to conduct a double materiality assessment. But where to start?

Download this free ebook to learn the key elements of the CSRD and the new EU Sustainability Reporting Standards, and see how to conduct a double materiality assessment in 5 simple steps.